Recent Post’s

Request a Call Back

Banks and Non-Banking Financial Companies (NBFCs) are the two major types of financial intermediaries in any financial system. The NBFCs are often private owned entities and when the government-owned entities are added, they are classified as NBFIs (Non-Banking Financial Intermediaries). NBFCs are mostly private owned financial institutions regulated by the RBI and other government entities. Both of them perform exceptional role in their respective domains. A comparison between the two is always important from the angle of monetary policy as well as the interest of depositors and investors.

In recent years, the RBI is putting high regulations on NBFCs. Some of the regulations are as hard as that of banks. Extension of the SARFAESI clause and putting more capital requirements are some of them. Actually, there is a trend of imposing almost all regulatory requirements of banks on the NBFC sector. This is because failure of big NBFCs is dangerous to the economy as well. The NBFCs are nicknamed as the shadow banking sector.NBFCs are regulated by the RBI under the RBI Act of 1935 from 1997 onward. They have to: register with the RBI, keep minimum capital, some of them have to maintain SLR and still some of them have to keep the CRAR (Capital to Risky Asset Ratio) etc. Other strict norms are also detailed by the RBI. Important NBFCs are identified by the RBI by categorizing them into systemically important NBFCs, deposit-taking NBFCs, NBFC- MFI etc.

What is an NBFC?

“A Non-Banking Financial Company (NBFC) is a company registered under the Companies Act, 1956 engaged in the business of loans and advances, acquisition of shares/stocks/bonds/debentures/securities issued by Government or local authority or other marketable securities of a like nature, leasing, hire-purchase, insurance business, chit business but does not include any institution whose principal business is that of agriculture activity, industrial activity, purchase or sale of any goods (other than securities) or providing any services and sale/purchase/construction of immovable property.” – RBI.

The Non-Banking Financial Companies are performing an exceptional role in the economy by delivering numerous type financial activities. NBFCs are actually a heterogeneous group providing several services extending from micro finance to insurance. They provide insurance, gives MFI loans, infrastructure financing etc.

Gold loan NBFCs, chit funds, Nidhi etc. are popular examples of NBFCs.

Features of NBFCs Are:

- The NBFCs are allowed to accept/renew public deposits for a minimum period of 12 months and maximum period of 60 months. They cannot accept deposits repayable on demand.

- The deposits with NBFCs are not insured.

- The repayment of deposits by NBFCs is not guaranteed by RBI.

Is there a lending difference between banks and NBFCs?

As far as lending is concerned banks tend to target corporates as well as retailers. On the other hand, NBFCs are more geared towards the retail sector. For example, this could be in vehicle finance, consumer loans etc. You do not see them lending to big power projects as an example. Another difference is in issue of credit cards. Banks tend to frequently issue credit cards of different types depending on the needs of the customers, while NBFCs do not.

Difference between Banks and Non-Banking Financial Companies

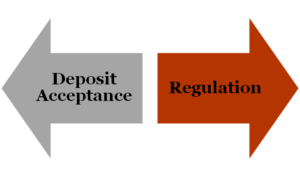

There are some notable differences as well as similarities regarding the functioning of the banks and NBFCs. First is from the angle of functioning and second from the angle of the extent of financial regulation by the RBI on both.

Deposit acceptance

Firstly, banks can do almost all financial services and products generally authorized to them. They can accept demand deposits (demand deposits have high liquidity and is considered as good as money). NBFCs can’t accept demand deposits.

The NBFCs can provide only specifies functions devoted to them. There is few deposit (other type of deposits) accepting NBFCs, but they are very strictly regulated by the RBI. The NBFCs are allowed to accept/renew public deposits for a minimum period of 12 months and maximum period of 60 months. There are only 254 deposit-taking NBFCs out of 12000 registered NBFCs. Regarding interest rate, the maximum rate of interest an NBFC can offer is 12.5%. The interest may be paid or compounded at rests not shorter than monthly rests. The repayment of deposits by NBFCs is not guaranteed by RBI.

Regulation

Second, from the angle of financial regulation, banks are strictly regulated by the RBI as they deal with public deposits. The NBFCs also have to follow RBI’s strict regulations but the extent of control is less compared to the banks. But in recent times, there is regulatory convergence between banks and NBFCs. This means that the regulatory norms are now coming look alike for both (though with slight differences). The following are the main differences between banks and NBFCs.

| Area | Banks | NBFCs |

| Demand Deposits | Can accept all types of deposits | Can’t accept demand deposits |

| Deposit insurance | Covered under the RBI’s deposit insurance. | No deposit insurance |

| Payment and Settlement system of the RBI | Banks are supported by the Payment and Settlement System (RTGS, NEFT etc.,) | Can not avail the payment and settlement system. |

| Foreign investment | Allowed up to 74% | Allowed up to 100% |

| CRR | Applicable | Not applicable |

| CRAR | Applicable | 15% CRAR for Deposit taking NBFCs and Non-Deposit taking – Systemically Important NBFCs. |

| SLR | Applicable | 15% SLR for Deposit taking NBFCs |

| SARFAESI | Applicable | Applicable |

| Provisioning | Applicable | Applicable |

| Incorporation | Banking Regulation Act | Companies Act (mostly) |

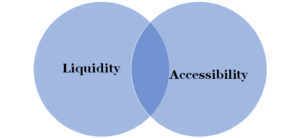

Why demand deposits acceptance is an important factor separating banks and NBFCs?

Demand deposit is a bank account which allows the account holder to withdraw his money from the account at his will and by any means without a notice to the bank. Demand deposits are unique because of two features:

Liquidity

The demand deposits balances are like ready to use money of the account holders in banks. Hence, they are usually considered as money and form the greater part of the narrowly defined money supply of a country. In the definition of Narrow Money, the demand deposits come as the main component. Here, from the monetary policy angle, demand deposit becomes very important. An institution that accepts demand deposits should be strictly controlled and regulated by the RBI. Hence, NBFCs which are nick named as shadow banks are not permitted to accept it.Similarly, when commercial banks issue cheques, it will lead to multiplier effect on money supply. Such power is absent for NBFCs as they can’t issue cheques.

Accessibility

The demand deposits can be accessible through any form (ATM, direct banking etc.). Hence the banks have to discharge them as soon and on the spot. Here also the NBFCs as a financial intermediary has limitations.